Table of Contents

- What is the One Big Beautiful Bill Act?

- Introduction: Understanding the One Big Beautiful Bill Act

- Why This Matters (Especially in PA & NY)

- Key Provisions of the One Big Beautiful Bill Act

- Key Provisions at a Glance

- How to Maximize Each Benefit

- Who Benefits and Who Doesn’t?

- Common Questions

- Maximizing Benefits Under the Act

- Plan with a CPA – Don’t Leave Money on the Table

- Frequently Asked Questions (FAQs)

- Conclusion

What is the One Big Beautiful Bill Act?

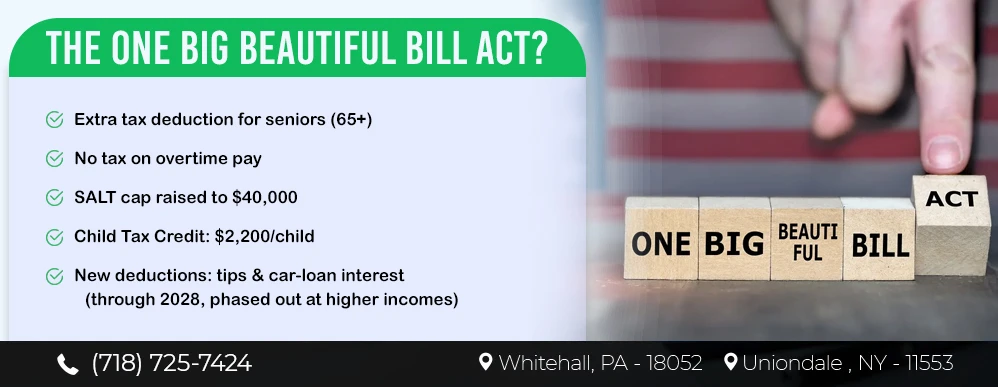

The One Big Beautiful Bill Act (H.R. 1), signed on July 4, 2025, delivers targeted federal tax relief. It introduces new tax deductions for seniors and working Americans, including an extra deduction for individuals aged 65+ and a “no tax on overtime” rule for workers. It also expands the SALT cap to $40,000 and raises the Child Tax Credit to $2,200 per child. Several new deductions – such as for tips and car-loan interest – apply through 2028, with phase-outs at higher incomes.

Introduction: Understanding the One Big Beautiful Bill Act

The One Big Beautiful Bill Act (OBBBA) is one of the most significant pieces of tax legislation in recent years. Signed into law in 2025, the Act provides targeted tax relief to working Americans and seniors while introducing new deductions and adjustments that impact both individuals and businesses. For taxpayers in Pennsylvania and New York, these changes present both opportunities and challenges that require careful tax planning with a trusted CPA.

Why This Matters (Especially in PA & NY)

Homeowners and high local-tax payers in Pennsylvania and New York may benefit from the higher SALT cap, while seniors and hourly workers can see meaningful reductions to taxable income. For many filers, these changes shift whether to take the standard deduction or itemize – and whether tracking overtime, tips, or vehicle financing could unlock new deductions.

Key Provisions of the One Big Beautiful Bill Act

1. Senior Tax Deduction

- Provides an additional $6,000 tax deduction for individuals aged 65 and older, available from 2025 through 2028.

- Married couples where both spouses qualify can claim up to $12,000.

- Benefit phases out for those with Modified Adjusted Gross Income (MAGI) over $75,000 (individuals) or $150,000 (joint filers).

2. No Tax on Overtime Rule

- Employees can deduct the “half-time” portion of their overtime pay.

- Caps at $12,500 for individuals and $25,000 for joint filers.

- Available until 2028.

- Phases out at higher incomes: begins at $150,000 (single) and $300,000 (MFJ), fully phased out around $400k/$550k.

3. Expanded SALT Deduction Cap

- Raises the state and local tax (SALT) deduction cap from $10,000 to $40,000.

- Applies through 2029 for taxpayers earning under $500,000.

- Phases down above $500,000 income.

- Reverts to $10,000 in 2030.

4. Child Tax Credit Adjustment

- Increases from $2,000 to $2,200 per child, indexed for inflation from 2026.

- The refundable portion remains unchanged.

- Phase-out thresholds remain at $200k (single) and $400k (MFJ).

5. No Tax on Tips

- Deduction of up to $25,000 of qualified cash tips from taxable income.

- Applies to traditionally tipped occupations.

- Income limits apply.

- Available 2025–2028.

6. Car-Loan Interest Deduction

- Deduction for qualifying personal auto loan interest, up to $10,000/year.

- Applies to loans after 12/31/2024.

- Must meet conditions: first-lien, personal-use, possible U.S. assembly rules.

- Leases excluded.

- Phase-outs begin near $100k (single) / $200k (MFJ).

- Available 2025–2028.

Key Provisions at a Glance

| Provision | What it does | Eligibility / Phase-outs | Effective Years |

|---|---|---|---|

| Senior Deduction | Additional $6,000 per person (above existing add-on) | Age 65+; phases out starting at $75k/$150k MAGI | 2025–2028 |

| No Tax on Overtime | Deduct half-time portion of overtime pay up to $25,000 | Requires SSN; phases out $150k/$300k; fully phased out ~$400k/$550k | 2025–2028 |

| No Tax on Tips | Deduct up to $25,000 in cash tips | Service-industry jobs; income limits apply | 2025–2028 |

| Car-Loan Interest | Deduct up to $10,000 personal auto loan interest | Loans after 12/31/24; leases excluded; income limits apply | 2025–2028 |

| SALT Deduction Cap | Raised from $10,000 to $40,000 | Phases down above $500k; reverts in 2030 | 2025–2029 |

| Child Tax Credit | Increased to $2,200 per child (indexed from 2026) | Phase-out at $200k/$400k; SSN rules apply | Begins 2025 |

How to Maximize Each Benefit

Seniors (65+)

- Claim the new $6,000 deduction per person – even if you don’t itemize.

- Mind MAGI phase-outs: partial benefits may still apply.

Employees Working Overtime

- Track hours and pay stubs carefully.

- Deduction applies to the overtime premium (the “half” in time-and-a-half).

- If income is near or above $150k/$300k, run projections.

Workers in Tipped Occupations

- Keep detailed, contemporaneous records for cash tips.

- Practical benefit depends on whether you owe federal income tax after standard deduction.

Car-Loan Interest Deduction

- Confirm loan and vehicle qualifications.

- Expect lender reporting via new 1098 forms.

- Save annual interest statements.

SALT Strategy (PA & NY)

- Only itemizers benefit.

- Run projections before year-end.

- Above $500k income, phasedown reduces benefit.

Who Benefits and Who Doesn’t?

Beneficiaries:

- Seniors with moderate incomes

- Middle-class families

- Employees with overtime pay

- Homeowners in PA & NY who itemize

- Service workers with documented tips

- Qualifying auto buyers who finance

Limited or No Benefit:

- Very low-income seniors and workers with no tax liability

- High-income households above phase-out thresholds

- Lessees or buyers of non-qualifying vehicles

- Non-itemizers who cannot claim SALT

Common Questions

Do I have to itemize to use SALT?

Can seniors claim the $6,000 deduction on top of the existing age-based deduction?

Is “no tax on overtime” exempt from payroll taxes?

Are electronic tips eligible?

What’s the new Child Tax Credit?

Maximizing Benefits Under the Act

While the OBBBA provides meaningful tax relief, the rules are nuanced. Taxpayers in Pennsylvania and New York should pay special attention to SALT deduction changes, as they stand to gain more than taxpayers in states with lower property taxes. Working Americans eligible for the overtime deduction should carefully track wages and hours to ensure they maximize their benefits.

Plan with a CPA – Don’t Leave Money on the Table

The new rules can change whether you itemize, how you structure compensation, and even when to buy a vehicle. Understanding and applying the provisions of the One Big Beautiful Bill Act requires professional guidance.

At Shah & Associates CPA, we help business owners, working professionals, and seniors in PA and NY plan strategically to minimize tax liability while staying fully compliant with IRS regulations. Whether it’s calculating senior deductions, optimizing overtime tax breaks, or navigating the SALT cap, our experienced CPA team ensures you don’t leave money on the table.

Ready to optimize your 2025–2028 taxes? Contact Shah & Associates CPA today to schedule a consultation. Let our expert team in Pennsylvania and New York guide you through these new tax provisions, maximize your savings, and ensure peace of mind.

Frequently Asked Questions (FAQs)

What is the One Big Beautiful Bill Act?

How does the senior deduction work?

What does “no tax on overtime” mean in practice?

Do I need to itemize to benefit from the SALT changes?

What’s the new Child Tax Credit?

Conclusion

The One Big Beautiful Bill Act brings both opportunities and complexities to U.S. taxpayers. By taking advantage of senior deductions, the no-tax-on-overtime rule, expanded SALT caps, and new deductions for tips and car-loan interest, many Americans can reduce their tax burden. However, because the rules vary based on age, income, and filing status, professional CPA tax planning is essential.

Contact Shah & Associates CPA today to schedule a consultation. Our team in Pennsylvania and New York will guide you through these new tax provisions, maximize your savings, and give you peace of mind.

Disclaimer: The information provided in this blog is for general educational and informational purposes only. It should not be considered tax, legal, or financial advice. Tax laws and regulations may change, and their application can vary based on your individual circumstances. For advice related to your specific situation, please consult with a qualified CPA, tax advisor, or financial professional before making any decisions.